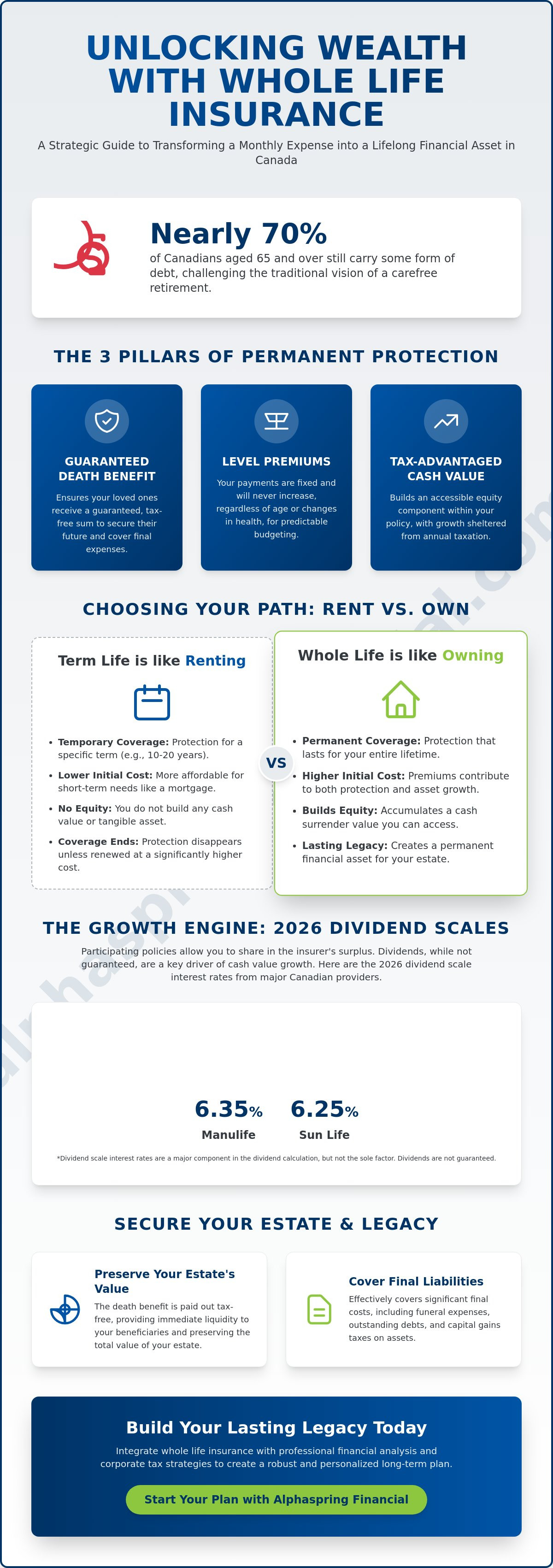

Did you know that nearly 70% of Canadians aged 65 and over still carry some form of debt in 2026? It's a sobering reality that challenges the traditional idea of a carefree retirement. You likely recognize that protecting your family requires more than just a temporary safety net, yet the higher premiums of whole life insurance Canada can feel like a significant hurdle. It's common to feel caught between the immediate affordability of term coverage and the complex growth structures of permanent policies.

This guide transforms that uncertainty into a strategic advantage by reframing insurance as a permanent financial asset rather than a monthly expense. You'll discover how the cash value component actually functions, with current 2026 dividend scales from major providers like Sun Life and Manulife reaching as high as 6.35%. We provide a logical framework to help you decide between term and permanent options, ensuring you realize the full potential of your estate. By the end, you'll have the clarity needed to manage estate taxes and secure a lasting legacy for your loved ones.

Key Takeaways

- Understand the three fundamental pillars of permanent protection: a guaranteed death benefit, level premiums, and the accumulation of tax-advantaged cash value.

- Learn how whole life insurance Canada functions as a strategic asset class by utilizing dividends to grow your policy's cash surrender value over time.

- Establish a clear framework to distinguish between the stability of whole life, the flexibility of universal life, and the temporary nature of term coverage.

- Discover how to leverage tax-free death benefits to preserve your estate's value and cover significant final liabilities like capital gains taxes.

- Realize how integrating insurance with professional financial analysis and corporate tax strategies creates a more robust and personalized long-term plan.

What is Whole Life Insurance in Canada?

Many people view insurance as a simple safety net for "just in case" scenarios. However, whole life insurance Canada functions more like a permanent financial foundation. It's a type of permanent life insurance that remains in effect for your entire lifetime, provided premiums are paid. Unlike other financial products that shift with market volatility, this policy offers a sense of calm through its structural guarantees. It's a steady presence in an often unpredictable financial world.

To understand its value, you should look at the three pillars that support every policy. First, there's the guaranteed death benefit, which ensures your loved ones receive a tax-free sum. Second, the level premium structure means your costs stay fixed. They don't increase as you age or if your health changes. Finally, the cash value component allows you to build equity within the policy. When you explore What is whole life insurance?, you see that the insurance company manages the underlying investments. They handle the complexity of the markets and the professional management of the participating account, while you benefit from the steady growth and stability of the asset.

The Permanent Promise: Coverage That Never Expires

Permanent protection means exactly what it says. Your coverage is guaranteed to pay out eventually, as long as the policy stays active. This certainty is vital for Canadians who want to ensure their final expenses and estate taxes are covered. Because the premiums never increase, you can plan your long-term budget with total confidence. This stability provides a necessary foundation for life insurance Canada, allowing you to focus on building a legacy instead of worrying about rising costs in your senior years.

Whole Life vs. Term Life: The Core Difference

Think of the difference between term and whole life as the difference between renting and owning a home. Term insurance is like renting. You pay for protection over a specific period, such as 10 or 20 years. It's affordable at the start, but when the term ends, the coverage disappears unless you renew at a much higher rate. You don't build any equity in the process. It's a temporary solution for temporary needs.

Whole life is like owning. Your initial costs are higher, but you're building a tangible asset. This equity, known as cash surrender value, belongs to you. You can eventually access it for opportunities, retirement income, or emergencies. Many Canadians find that a strategic mix works best. They use term insurance to cover temporary debts like mortgages and whole life insurance Canada to handle permanent needs like estate planning and legacy gifts. This balanced approach ensures you have the right protection for every stage of your life.

The Mechanics of Cash Value and Dividends

One of the most compelling reasons to choose whole life insurance Canada is the accumulation of cash surrender value (CSV). This isn't just a ledger entry. It's a tangible, accessible asset that grows over time. While the death benefit provides for your heirs, the cash value provides for you during your lifetime. Under current Canada Revenue Agency (CRA) rules, the growth within your policy remains tax-sheltered as long as it stays within the "exempt test" limits. This allows your wealth to compound more efficiently than it would in a fully taxable account.

Understanding how this growth happens requires a look at the difference between participating and non-participating policies. A non-participating policy offers fixed, guaranteed growth but does not share in the insurer's success. In contrast, participating policies allow you to receive dividends. These dividends represent a share of the "surplus" generated by the insurance company's participating account. According to the Financial Consumer Agency of Canada guide, these accounts are managed conservatively to ensure long-term stability, even when the broader stock markets are volatile.

Participating Policies: Earning Dividends

The "Par Account" acts as a massive pool of professionally managed assets. In 2026, major Canadian insurers continue to demonstrate the strength of these accounts. For instance, Sun Life’s dividend scale interest rate is 6.25% as of April 1, 2026, while Manulife’s rate stands at 6.35%. Participating dividends are essentially a return of a portion of the premiums you paid, representing your share of the insurer’s surplus. You have several options for these dividends. You can take them as cash, use them to reduce your annual premiums, or purchase "paid-up additions" to increase your total death benefit and cash value over time.

Accessing Your Equity: Loans and Withdrawals

Your policy's cash value can serve as a flexible "private bank" for strategic opportunities. If you need capital for a business expansion or an emergency, you can take a policy loan. The insurance company uses your cash value as collateral, meaning your underlying investment continues to grow. As of April 2026, the interest rate for borrowing against an RBC Insurance whole life policy is 6.45%. This is often more efficient than a traditional bank loan. While withdrawals may have tax implications if they exceed your adjusted cost basis, loans are generally not considered taxable income. If you're curious about how these mechanics fit into your specific situation, a professional financial analysis can help clarify your options.

Whole Life vs. Universal Life vs. Term

Selecting the right path for your family's security requires a clear understanding of how different policies behave over decades. While whole life insurance Canada offers a "hands-off" approach with guaranteed growth, other options introduce variables that may or may not align with your risk tolerance. You aren't just buying a death benefit. You're choosing a financial structure that will either require active management or provide a steady, predictable floor for your estate.

Universal life (UL) is often presented as a flexible alternative, allowing you to adjust premiums and choose your own investment accounts. However, this flexibility comes with significant responsibility. In a fluctuating interest rate environment, UL policies carry the risk of "imploding" if the underlying investments fail to cover the rising internal costs of insurance. If returns lag, you might be forced to inject large sums of capital just to keep the coverage active. Whole life removes this uncertainty by placing the investment risk on the insurer rather than the policyholder.

Comparison Framework for Canadian Families

To help you visualize these differences, consider how each policy type handles the core components of your plan:

| Feature | Term Life | Universal Life | Whole Life |

|---|---|---|---|

| Premium Stability | Fixed for term | Flexible but can rise | Guaranteed Level |

| Cash Value Growth | None | Market-dependent | Guaranteed & Dividends |

| Investment Risk | None | Policyholder assumes risk | Insurer assumes risk |

| Duration | Temporary (e.g., 20 years) | Permanent | Permanent |

Choosing Based on Your Life Stage

Your current milestones often dictate which strategy makes the most sense. Young families typically start with term insurance. It provides the maximum amount of coverage for the lowest initial cost, protecting high-exposure years involving mortgages and young children. It's a practical solution for a temporary need.

As you become an established professional or business owner, the conversation shifts toward tax efficiency and wealth preservation. This is where whole life insurance Canada becomes a strategic corporate or personal asset. Business owners often use these policies to create a tax-sheltered "sinking fund" that can be used for buy-sell agreements or as a stable collateral source for future loans. By integrating this coverage with a comprehensive financial analysis and forecasting, you ensure that your insurance isn't just a cost, but a functional part of your broader accounting and tax strategy.

Strategic Benefits: Tax Efficiency and Estate Planning

A well-structured estate plan is about more than just distributing assets. It's about ensuring those assets actually reach your heirs without being depleted by the CRA. In this context, whole life insurance Canada serves as a high-efficiency tool for managing final liabilities. While other investments are subject to capital gains or income taxes, the death benefit from a life insurance policy is paid out entirely tax-free. It provides the liquidity your estate needs exactly when it's needed most.

This liquidity is particularly vital for estate equalization. If you intend to leave a family business or a vacation property to one child, you may struggle to provide an equivalent value to your other heirs. Life insurance solves this imbalance. It allows you to gift the physical asset to one person while providing a tax-free cash legacy to others. This prevents family friction and ensures everyone feels valued in your final plan.

Solving the 2026 Estate Tax Challenge

As property values across Canada continue to rise in 2026, many families face a significant tax trap at the time of death. The CRA treats secondary properties and non-registered investments as if they were sold on the date of your passing, triggering immediate capital gains taxes. Without a dedicated source of cash, your executors might be forced to sell the family cottage just to pay the tax bill. Because the death benefit is paid directly to your named beneficiaries, it bypasses the delays and costs of probate. This provides immediate, accessible funds to settle your affairs without liquidating precious family assets.

The Corporate Advantage

For business owners, the strategic use of whole life insurance Canada offers a unique way to manage corporate surplus. When a corporation owns the policy, the death benefit proceeds (minus the adjusted cost basis) flow into the company's Capital Dividend Account (CDA). This special account allows you to distribute funds to shareholders as tax-free dividends. It's one of the most efficient ways to move wealth out of a corporation and into the hands of your family. Beyond the tax benefits, the growing cash value also strengthens your company’s balance sheet, providing a stable asset that can be used for future business needs. If you want to optimize your corporate structure, you can explore the approach to wealth management Canada provided by Alphaspring Financial Inc.

Ready to protect your estate from unnecessary tax erosion? Consult with an expert at Alphaspring Financial Inc. to align your insurance with your long-term legacy goals.

How to Build Your Legacy with Alphaspring Financial Inc.

Effective estate planning begins with a comprehensive understanding of your current financial landscape. At Alphaspring Financial Inc., we don't believe in off-the-shelf solutions or generic advice. We recognize that whole life insurance Canada is a sophisticated instrument that must be tuned to your specific goals. Our process starts with a holistic financial analysis. We look beyond the policy itself to see how it interacts with your existing assets, liabilities, and future aspirations. This methodical approach ensures that every recommendation we make is grounded in data and designed for long-term stability.

A common challenge for many Canadians is the lack of coordination between their insurance agent and their accountant. We bridge this gap by integrating your insurance strategy with your broader tax and accounting framework. Because we offer dual expertise in both life insurance and corporate tax, we can identify opportunities that others might miss. Whether you're using a policy to fund a buy-sell agreement or to create a tax-efficient retirement stream, our meticulous planning helps you avoid the pitfalls of a fragmented strategy. You gain a unified plan that works together to protect your wealth and your family.

A Tailored Perspective on Permanent Protection

Our discovery process is designed to find the right "fit" for your unique circumstances. We analyze your corporate structure and personal portfolio to determine how much permanent protection is necessary to meet your legacy goals. This isn't about high-pressure sales. It's about professional consulting that respects your milestones. By aligning whole life insurance Canada with your corporate tax obligations, we help you transform a necessary protection into a strategic asset. Our goal is to provide a bespoke experience that reflects the serious nature of your wealth management needs.

Securing Your Future Today

Time is a critical factor in any permanent insurance strategy. Locking in your rates while your health and age are favourable ensures the most cost-effective foundation for your estate. Waiting even a few years can significantly impact the long-term growth of your cash value and the total cost of your coverage. We invite you to begin the conversation with a portfolio review. By booking a consultation with an advisor at Alphaspring Financial Inc., you take the first step toward a more secure and predictable future. You don't have to manage these complexities alone. We're here to act as your wise guide, providing the steady, reliable presence you need to achieve true peace of mind. Contact Alphaspring Financial Inc. today to start building your lasting legacy.

Securing Your Lasting Legacy with Confidence

Choosing the right protection is more than a simple transaction; it's a commitment to your family's long-term stability. You've seen how whole life insurance Canada acts as a permanent financial floor, offering guaranteed growth and significant tax advantages for your estate. Whether you're managing corporate surplus or protecting a family cottage, the right structure ensures your hard-earned assets remain intact for the next generation. This strategic foresight transforms a monthly premium into a powerful, multi-generational asset that provides certainty in an unpredictable world.

Since 2017, Alphaspring Financial Inc. has focused on holistic wealth optimization with specialized dual expertise in insurance and corporate tax advisory. We provide national service coverage across Canada, offering the meticulous planning needed to turn complex financial challenges into clear, actionable strategies. It's time to move beyond generic solutions and embrace a plan designed specifically for your life milestones and family goals. Connect with an advisor at Alphaspring Financial Inc. to design your permanent legacy plan and gain the peace of mind that comes from true foresight. Your family's future deserves a foundation built on stability and proven expertise.

Frequently Asked Questions

Is whole life insurance worth it for Canadians in 2026?

Yes, it is worth it for those seeking permanent security and tax-advantaged growth. It serves as a stabilized asset class that provides a financial floor for your estate. While initial costs are higher, the long-term benefits of a guaranteed payout and accessible equity often outweigh the premium expense for established professionals or those with permanent tax liabilities.

How does the cash value grow in a Canadian whole life policy?

Cash value in a whole life insurance Canada policy grows through a combination of guaranteed annual increases and potential dividends. The insurance company manages a large pool of assets in a participating account, and a portion of the growth is credited to your policy. This accumulation remains tax-sheltered within the policy's exempt limits, allowing your equity to compound efficiently over several decades.

Can I cancel my whole life insurance and get my money back?

You can cancel your policy at any time and receive the cash surrender value accumulated to that date. It's important to realize that in the early years of a policy, the surrender value may be minimal because of initial administrative and underwriting costs. You should review your policy's specific table of values to understand the exact amounts available at each contract anniversary.

What is the average cost of whole life insurance in Canada?

The cost varies significantly based on your age, health status, and the amount of coverage you choose. Generally, premiums for whole life insurance Canada are five to ten times higher than term insurance because the coverage is permanent and builds equity. However, these premiums are guaranteed to remain level for life, protecting you from the significant price increases typically associated with aging.

How are dividends calculated on participating life insurance?

Dividends are calculated based on the performance of the insurance company’s participating account. The insurer evaluates three main factors: investment returns, mortality experience, and operational expenses. If the company performs better than originally projected in these areas, a portion of that surplus is distributed to participating policyholders as a dividend, though these are not guaranteed.

Can I use my whole life insurance to fund my retirement?

Yes, you can access your policy's equity to supplement your retirement income. Many Canadians use policy loans or collateral assignments to access cash without triggering immediate tax consequences. This strategy allows your underlying assets to continue growing while you enjoy a flexible, stable source of funding for your lifestyle or unexpected retirement expenses.

What happens if I stop paying premiums on my whole life policy?

If you stop paying, the policy may stay active through an automatic premium loan if there's enough cash value to cover the cost. You might also choose to convert the policy to a reduced paid-up status, which provides a smaller death benefit with no further premiums required. If no cash value exists, the coverage will simply lapse after a standard thirty-day grace period.

Is the death benefit from whole life insurance taxable in Canada?

The death benefit is typically paid out to your named beneficiaries completely tax-free. This remains one of the most significant advantages of life insurance in Canada. It provides an immediate, liquid sum that can be used to settle estate debts or provide for heirs without the erosion caused by income or capital gains taxes.