What if the greatest risk to your retirement isn't the size of your portfolio, but the way you choose to dismantle it? Most Canadians spend decades focused on accumulation, yet the true challenge lies in the transition to decumulation. Effective retirement income planning is no longer just about saving; it's about the precision of your withdrawal architecture. You've worked hard to build your RRSPs and TFSAs. Now, you need a strategy that ensures those assets don't vanish into unnecessary taxes or trigger an avoidable OAS clawback when your net income exceeds $93,454.

It's natural to feel uneasy about market volatility or the complex choice of when to start your CPP. You want to feel certain that your spouse is protected and that you're maximizing every government benefit you've earned. We'll show you the exact steps to bridge the gap between your savings and a sustainable monthly paycheque. This guide outlines a tax-efficient withdrawal sequence, explains how to utilize your 2026 TFSA limit of $7,000, and demonstrates how to coordinate your private assets for total peace of mind.

Key Takeaways

- Define your personal income gap. Calculate the difference between guaranteed pensions and your desired lifestyle costs to ensure your plan remains resilient against 2026 inflation trends.

- Coordinate your OAS and CPP benefits. Learn how to time these payments so you don't lose your hard-earned income to avoidable government clawbacks.

- Prioritize tax efficiency. Implement a strategic withdrawal sequence that helps you master the complexities of retirement income planning while keeping more of your money.

- Move beyond the RRSP. Discover why incorporated professionals often find traditional limits insufficient and how an Individual Pension Plan (IPP) offers a more tailored solution.

- Protect your cash flow. Safeguard your monthly income against unexpected medical costs by integrating health and dental insurance into your holistic financial roadmap.

Understanding the Retirement Income Gap in 2026

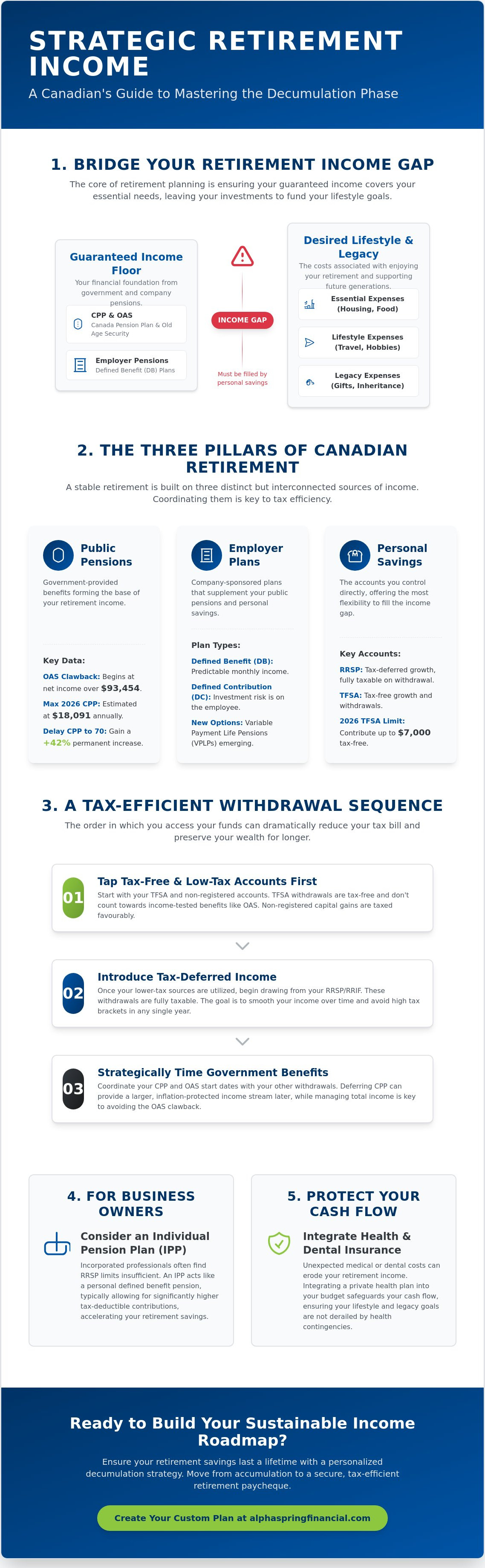

Retirement isn't just a date on a calendar; it's a structural shift in how you manage your wealth. The retirement income gap represents the shortfall between your guaranteed monthly income, such as CPP and OAS, and your actual monthly expenses. In 2026, this gap is widening for many Canadians. Persistent inflationary pressures mean that yesterday's nest egg must stretch much further today. Mastering retirement income planning requires you to look beyond your total savings and focus on the reliability of your monthly cash flow.

To better understand how market structures influence your long-term returns and income potential, watch this helpful video from Morningstar:

We typically categorize retirement spending into three distinct buckets to create clarity. First, essential expenses cover your housing, food, and utilities. These are non-negotiable costs. Second, lifestyle expenses include travel, hobbies, and dining. Finally, legacy expenses involve the funds you wish to set aside for the next generation. Creating a guaranteed income floor to cover your essentials provides the psychological stability needed to enjoy your lifestyle goals without constant market anxiety.

Calculating Your Real Retirement Needs

Many people mistake their pre-retirement gross salary for their post-retirement needs. While you won't be paying into CPP or EI anymore, your tax bracket will shift. You must account for the Go-Go, Slow-Go, and No-Go phases of aging. Early retirement often sees higher spending on travel and leisure, while later years may require significant funds for health contingencies. Integrating robust health and dental insurance into your plan ensures that unexpected medical costs don't erode your lifestyle budget or force you to dip into capital prematurely.

The Role of Inflation and Purchasing Power

Inflation is the silent predator of a fixed income. Even a modest 3% inflation rate can cut your purchasing power significantly over a 30-year retirement. This is why we distinguish between nominal income, which is the dollar amount you receive, and real income, which is what those dollars actually buy. Comprehensive Retirement planning in 2026 demands that you over-estimate your future needs. You need to ensure the colour of your money stays vibrant even as the cost of living rises. Relying on a static plan is risky; a dynamic approach that accounts for retirement income planning adjustments is the only way to maintain your standard of living.

The Three Pillars of Canadian Retirement Income

A reliable retirement strategy stands on three foundational pillars. These Canadian retirement income sources include public pensions, employer-sponsored plans, and your personal savings. While each pillar provides a separate stream of cash, they are deeply interconnected. Poor coordination often leads to higher tax brackets or the loss of government benefits. Effective retirement income planning ensures that your withdrawals are sequenced to preserve your wealth rather than deplete it through inefficiency.

Employer-sponsored plans often serve as the middle pillar. Defined Benefit (DB) plans offer a predictable monthly amount, while Defined Contribution (DC) plans leave the investment risk with you. As of January 1, 2026, new options like Variable Payment Life Pensions (VPLPs) are becoming available in certain jurisdictions, offering fresh ways to secure periodic income. Understanding the limitations of these workplace plans is essential for determining how much your personal savings must provide to cover the remaining gap.

Maximizing Government Benefits

Timing is vital for the Canada Pension Plan (CPP) and Old Age Security (OAS). For 2026, the maximum annual CPP retirement benefit is $18,091. Choosing to delay your CPP until age 70 results in a 42% permanent increase in your monthly payment. This guaranteed, inflation-indexed boost acts as a powerful hedge against longevity. However, you must stay mindful of the 2026 OAS clawback threshold. If your 2025 net income exceeds $93,454, the government begins to recover these benefits. A professional financial analysis can help you navigate these thresholds without sacrificing your retirement lifestyle.

Private Savings and the RRIF Transition

Your RRSP eventually reaches a strategic turning point. By December 31 of the year you turn 71, you must convert these savings into a Registered Retirement Income Fund (RRIF) or an annuity. This transition introduces mandatory minimum withdrawals that are fully taxable. If these withdrawals push your income too high, you risk triggering the OAS recovery tax. In contrast, the Tax-Free Savings Account (TFSA) remains a vital tool for flexibility. With a 2026 contribution limit of $7,000, the TFSA allows you to pull funds for major purchases or travel without affecting your taxable income or pension eligibility. Strategic retirement income planning uses the TFSA as a pressure valve to keep your total taxable income within the lowest possible bracket.

How to Build Your Withdrawal Strategy: A Step-by-Step Guide

Turning a lifetime of savings into a consistent monthly paycheque requires more than just a bank transfer. It demands a methodical sequence. While most investors focus on the total value of their portfolio, the true success of retirement income planning depends on how you dismantle those assets. A well-constructed withdrawal strategy protects your capital from excessive taxation and ensures your money lasts as long as you do. Follow these five steps to build your roadmap.

- Step 1: Define your net gap. Start with your baseline lifestyle costs. Subtract your guaranteed income from CPP and OAS. The remaining amount is what your private savings must generate each month.

- Step 2: Target the lowest tax bracket. For 2026, the first federal tax bracket is 14% on income up to $58,523. Aim to fill this bracket first to keep your effective tax rate as low as possible.

- Step 3: Prioritize non-registered assets. Generally, you should deplete taxable non-registered accounts first. This allows your RRSPs and TFSAs to benefit from additional years of tax-sheltered growth.

- Step 4: Manage the OAS recovery tax. Monitor your total income to stay below the 2026 OAS clawback threshold of $93,454. If you're nearing this limit, use TFSA withdrawals to meet your cash needs without increasing your taxable income.

- Step 5: Review and rebalance. Your plan must be dynamic. Conduct an annual financial consulting session to adjust for market performance and changes in your personal goals.

The Tax-Efficiency Hierarchy

The standard withdrawal order isn't always the most effective for high-income earners. In some scenarios, an "RRSP meltdown" is more beneficial. This involves taking larger RRSP withdrawals before age 71 to reduce the size of future mandatory RRIF payments. By doing this, you avoid being pushed into a much higher tax bracket later in life. Additionally, utilizing dividend tax credits in your non-registered accounts can significantly lower your effective tax rate compared to interest-bearing investments.

Managing Market Volatility (Sequence of Returns Risk)

The most dangerous time for your portfolio is the first few years of retirement. A significant market drop during this period, known as sequence of returns risk, can permanently impair your capital if you're forced to sell assets at a loss. To mitigate this, we recommend a "Cash Buffer" strategy. Keep at least two years of your lifestyle expenses in liquid, low-risk assets. This ensures you don't have to liquidate equities during a market downturn, giving your portfolio the time it needs to recover while your lifestyle remains uninterrupted.

Specialized Strategies for Business Owners and Incorporated Professionals

Incorporated professionals often find that traditional savings vehicles fall short of their long-term goals. For 2026, the maximum RRSP contribution is $33,810. While this is a significant amount, it's often insufficient for high-earning business owners who need to replace a substantial income. Advanced retirement income planning for business owners requires a shift from personal savings to corporate-integrated strategies. By leveraging your corporation, you can build a more robust and tax-efficient retirement foundation.

The decision between taking a salary or dividends is more than just a year-end accounting choice. It dictates how much RRSP room you create and affects your future CPP entitlements. Our corporate tax services help you find the optimal balance to maximize your current cash flow while securing your future. Converting business equity into a sustainable retirement paycheque involves careful succession planning and a clear understanding of how to extract corporate wealth without triggering excessive tax liabilities.

The IPP Advantage

An Individual Pension Plan (IPP) for incorporated professionals offers a powerful alternative to the RRSP. Designed for owners over age 40, IPPs allow for significantly higher contribution limits that increase as you age. Your corporation can also make "past service" contributions to catch up on previous years of employment. Beyond the tax advantages, IPPs provide a predictable retirement outcome and a high level of creditor protection, ensuring your legacy remains secure regardless of business fluctuations.

Corporate Surplus and Passive Income Rules

Managing the wealth within your Canadian Controlled Private Corporation (CCPC) requires precision. You must navigate the $50,000 passive income threshold to avoid losing access to the small business tax rate. Strategic retirement income planning involves extracting corporate surplus in a way that minimizes your personal tax hit. This often includes utilizing corporate-owned life insurance as a tool for both estate planning and tax-sheltered growth. These bespoke solutions allow you to protect your family while creating a stable, tax-efficient stream of income that isn't solely dependent on your business operations.

Finalizing Your Sustainable Income Roadmap

Creating a sustainable paycheque is more than a mathematical exercise. It's a commitment to your future self. While we've explored tax brackets and withdrawal sequences, a truly resilient roadmap must account for the variables you cannot control. Integrating health and dental insurance into your plan is a vital step to prevent lifestyle leakage. Without this protection, a single unforeseen medical event can force you to withdraw extra funds from your RRIF, potentially triggering higher taxes and eroding your capital prematurely. Strategic retirement income planning ensures that your lifestyle remains uninterrupted by these hidden costs.

A holistic approach is the only way to achieve lasting security. You must coordinate your investment returns with your insurance coverage and your corporate tax obligations. This level of coordination is complex. It's exactly why retirement planning in Canada requires a wise guide to navigate the shifting regulations of 2026. Transitioning from the theory of saving to the reality of spending requires a partner who understands the personal nature of your family goals and the technical details of your wealth.

Risk Management Beyond the Portfolio

Longevity is a risk that requires meticulous foresight. While living to 100 is a significant milestone, it necessitates a plan that doesn't run dry at age 85. Critical illness and disability insurance provide a necessary safety net that protects your portfolio from being raided during a health crisis. These tools ensure that your retirement income remains dedicated to your lifestyle rather than medical bills. This protection also offers a reassuring presence for a surviving spouse, guaranteeing that they remain financially secure and supported regardless of what the future holds.

The Alphaspring Financial Inc. Collaborative Approach

Our team brings together professional accounting, corporate tax expertise, and financial consulting to simplify your transition into retirement. We don't believe in one-size-fits-all solutions. Instead, we offer a bespoke experience where every detail of your withdrawal architecture is handled with meticulous care. We help you move from the anxiety of uncertainty to the calm of a structured, tax-efficient roadmap. Your future deserves a plan that is as unique as the career you've built. Take the first step toward a secure, predictable retirement paycheque today. Schedule a consultation with Alphaspring Financial Inc. to secure your future and realize the peace of mind that comes with a professionally crafted plan.

Taking Control of Your Financial Legacy

The transition from accumulation to decumulation is a significant life milestone that requires meticulous care. You've seen how coordinating your government benefits with private assets can protect you from the OAS clawback. You also understand that for business owners, standard limits are often just the starting point. Effective retirement income planning isn't a one-time event; it's a dynamic process that balances tax efficiency with long-term protection. By aligning your insurance, investments, and tax planning, you can replace uncertainty with a sense of calm.

Since 2017, Alphaspring Financial Inc. has focused on providing stability through a unique combination of corporate tax expertise and wealth management. We specialize in bespoke strategies for incorporated professionals, ensuring every detail of your roadmap is handled with quiet confidence. You don't have to navigate these complexities alone. A professional, integrated approach ensures that your spouse is protected and your lifestyle remains secure. Secure your retirement income with a tailored plan from Alphaspring Financial Inc. today. Your future is built on the decisions you make now. Let's make them count together.

Frequently Asked Questions

What is the best age to start taking CPP in Canada?

The ideal age to begin your Canada Pension Plan (CPP) depends on your health, longevity, and other income sources. While you can start as early as age 60 at a reduced rate, delaying until age 70 provides a permanent 42% increase in your monthly payment. This guaranteed, inflation-indexed boost is often the most effective way to secure your long-term purchasing power if you have sufficient private savings to bridge the early years.

How does the OAS clawback work in 2026?

The Old Age Security (OAS) clawback, or recovery tax, begins when your 2025 net income exceeds $93,454. For every dollar earned above this threshold, the government recovers 15 cents of your OAS benefit through your tax return. Careful retirement income planning is necessary to sequence withdrawals from your RRIF and non-registered accounts so that you don't inadvertently trigger this significant reduction in your government pension.

Should I withdraw from my TFSA or RRSP first in retirement?

You should generally withdraw from your taxable non-registered accounts first to allow your registered plans to continue growing tax-sheltered. Once those are depleted, we recommend withdrawing from your RRSP or RRIF up to the top of your current tax bracket. Your TFSA should be used as a flexible tool for larger, one-time expenses because these withdrawals don't count as taxable income and won't affect your eligibility for government benefits.

Can I still contribute to an RRSP after I retire?

You can continue making RRSP contributions as long as you have earned income and available contribution room. This is possible until December 31 of the year you turn 71, at which point the plan must be converted to a RRIF or annuity. If you're still working part-time or have rental income that qualifies as earned income, these contributions remain an effective way to lower your taxable income during your transition years.

What is an Individual Pension Plan (IPP) and is it better than an RRSP?

An Individual Pension Plan (IPP) is a defined benefit pension plan designed specifically for business owners and incorporated professionals. For those over age 40, an IPP typically allows for much higher contribution limits than a standard RRSP. It provides greater creditor protection and allows your corporation to make tax-deductible contributions for past service, making it a sophisticated alternative for those with high professional earnings.

How much can I withdraw from my RRIF each year?

There is no maximum limit on RRIF withdrawals, but you must take out a mandatory minimum percentage annually starting the year after you open the account. For example, if you're 72, the minimum withdrawal rate is approximately 5.40%. These withdrawals are considered fully taxable income. Strategic retirement income planning involves balancing these mandatory amounts with other income streams to avoid being pushed into a higher tax bracket unnecessarily.

What happens to my retirement income if the stock market crashes?

A well-structured plan utilizes a cash buffer to protect your lifestyle from market volatility. By keeping at least two years of expenses in liquid, low-risk accounts, you don't have to sell equities while prices are low. This approach provides the time your portfolio needs to recover. Having this stability in place ensures that a temporary market downturn doesn't become a permanent threat to your long-term financial security.

Do I need life insurance during my retirement years?

Life insurance remains a critical tool in retirement for estate planning and tax management rather than just income replacement. It can be used to cover terminal tax liabilities on secondary properties or to ensure a legacy is left for your children and grandchildren. Maintaining coverage provides peace of mind that your final expenses and taxes won't become a burden for your surviving spouse or heirs during a difficult time.