What if the greatest threat to your long-term financial security isn't a market shift, but the quiet accumulation of routine medical expenses? While we value our provincial systems like OHIP and AHCIP, many professionals and families realize that the healthcare we rely on leaves significant gaps for prescription drugs and dental procedures. You likely feel that the complexity of insurance jargon only adds to the uncertainty of protecting your family's health. Securing the right health and dental insurance Canada plan is a strategic move that transforms an unpredictable expense into a manageable, tax-efficient tool for wealth preservation.

This guide will help you bridge the gap between basic provincial coverage and your personal requirements with a clear, strategic comparison of the leading options available in 2026. We will examine the latest Canadian Dental Care Plan (CDCP) renewal requirements and the co-payment structures that impact your family's net income. You will gain a methodical understanding of coverage tiers and learn how to select a plan that offers high utility for routine care while providing peace of mind against catastrophic drug costs. By the end of this article, you will have the foresight needed to choose a bespoke solution that aligns with your professional goals and family milestones.

Key Takeaways

- Understand the specific limitations of provincial healthcare systems to ensure your family is protected against the rising costs of specialty prescriptions.

- Contrast the flexibility of individual policies with the stability of group benefits to secure the most effective health and dental insurance Canada provides for your specific career stage.

- Determine how to evaluate coverage categories like restorative dental and generic drugs to ensure your policy delivers a high return on your investment.

- Discover how to utilize health insurance premiums as a strategic, tax-efficient tool within your overall financial and wealth management plan.

- Gain the clarity needed to bridge the gap between basic government coverage and a bespoke protection plan that safeguards your long-term financial legacy.

Navigating the Provincial Gap: Why Supplementary Health Insurance is Essential in 2026

Many residents believe that provincial coverage is a comprehensive shield. However, the reality of Canada's public healthcare system is that it focuses primarily on hospital and physician services. This leaves a significant portion of daily wellness costs to the individual. As we move through 2026, the cost of specialty drugs and advanced dental procedures continues to outpace inflation. Securing health and dental insurance Canada is no longer just a luxury for the risk-averse; it's a vital component of a stable financial plan that protects your family's future.

To understand how these plans bridge the gap for Canadian families, watch this overview of how comprehensive coverage functions:

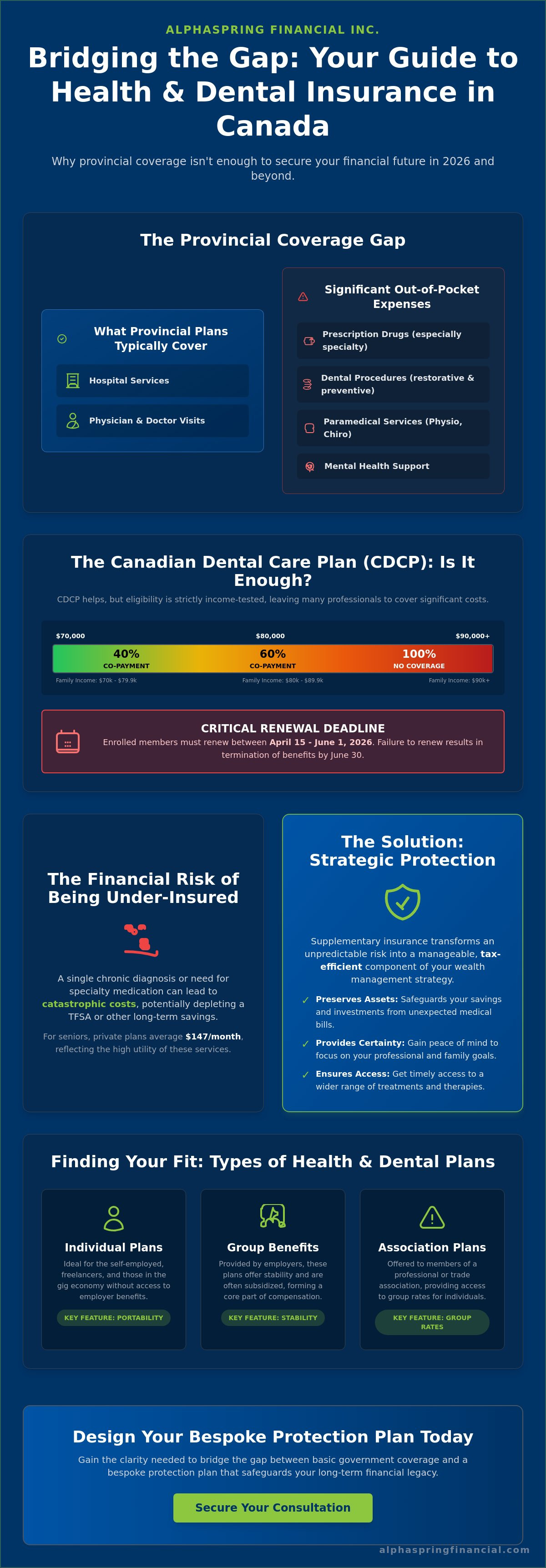

The landscape is shifting with the expansion of the Canadian Dental Care Plan (CDCP). While this federal initiative aims to help, it's strictly income-tested. Families with an adjusted net income between $70,000 and $79,999 still face a 40% co-payment, while those between $80,000 and $89,999 must cover 60% themselves. If your family earns $90,000 or more, you remain entirely responsible for these costs. For those already enrolled, the renewal window between April 15 and June 1, 2026, is a critical deadline. Missing this window results in a termination of benefits by June 30. Supplementary insurance acts as a buffer, ensuring that medical needs don't force you to liquidate long-term assets or stall your progress.

Common Out-of-Pocket Expenses in Canada

Prescription drugs are a primary concern. While National Pharmacare progress is being made, it's currently limited to specific areas like diabetes medication. For many, the cost of specialty drugs for chronic conditions remains a private burden. Routine dental work also sees rising costs, with basic preventive care becoming more expensive as clinical overheads increase. Paramedical services like physiotherapy and mental health support are also essential, yet they're rarely covered by provincial plans. Private plans for seniors average around $147 per month, reflecting the higher utility and necessity of these services as we age.

The Financial Risk of Being Under-Insured

One chronic diagnosis can quickly deplete a Tax-Free Savings Account (TFSA). For a family without a plan, a sudden need for specialty medication can cost thousands of dollars per year. This "catastrophic cost" is a risk that few can afford to ignore. Beyond the dollars, there's a profound psychological value in certainty. Knowing that your health and dental insurance Canada coverage is in place allows you to focus on your professional growth and family milestones. It removes the constant worry of an unexpected medical bill and provides a composed, future-focused atmosphere for your household.

Comparing Your Options: Individual, Group, and Association Health Plans

Selecting the right framework for your coverage is a strategic decision that depends on your employment status and long-term goals. Not all plans are built on the same foundation. While some prioritize the flexibility of the individual, others utilize the collective strength of a larger workforce. Securing the right health and dental insurance Canada plan requires a methodical look at how these structures differ. For those in the gig economy or running a freelance consultancy, individual plans provide essential portability. Your coverage remains constant even if you change clients or projects. Conversely, group benefits remain the gold standard for many business owners and employees. They leverage collective bargaining power to provide deeper coverage limits that are often difficult to obtain on an individual basis.

Professionals such as engineers, teachers, or accountants often have access to a third option: association plans. These plans allow individuals to pool their risks with other members of their professional order. This often results in a middle ground between individual flexibility and group-rate efficiency. Before making a choice, you must decide between a guaranteed issue plan and one that is medically underwritten. Underwritten plans require a health questionnaire but often reward good health with lower premiums or higher coverage ceilings. Speaking with a consultant at Alphaspring Financial Inc. can help you navigate these nuances to find a plan that mirrors your specific career trajectory.

Individual vs. Group Benefits: A Strategic Comparison

The primary difference between these models lies in the cost-sharing structure. In a group environment, the employer typically pays a significant portion of the premium. This makes it an incredibly cost-effective way to access high-tier dental and drug limits. For the self-employed, individual plans require you to cover the full premium, but they offer the advantage of being fully tailored to your family's needs. You should also consider the tax advantages for health plans as defined by the Canada Revenue Agency. In many cases, these premiums can be structured as a legitimate business expense or a medical tax credit, which improves your overall return on investment.

Guaranteed Acceptance: Protection Without the Paperwork

Guaranteed issue plans are a reliable solution for those who want to avoid medical questions. They are particularly useful if you have a pre-existing condition that might lead to exclusions in a standard plan. While premiums for these plans are sometimes higher, they offer immediate peace of mind. Many Canadians use the "FollowMe" concept when leaving a corporate job. This allows you to transition from a group plan to an individual policy without a medical exam, provided you apply within a specific window, usually 60 to 90 days. For those seeking immediate protection, it is vital to note that some private providers require applications by May 31, 2026, for coverage to begin on June 1. You should be aware that these plans often have initial waiting periods or lower caps for major dental work and orthodontics during the first year of coverage. This methodical approach ensures the insurer can maintain stability while still providing you with a vital safety net.

The Anatomy of a Policy: Key Coverage Categories to Evaluate

Understanding the specific layers of a policy is vital for ensuring your protection matches your life stage. A one-size-fits-all approach rarely suffices when managing complex health needs. When evaluating health and dental insurance Canada options, you must look beyond the monthly premium to the specific maximums and co-insurance percentages. These details determine your actual out-of-pocket costs during a claim. For instance, prescription drug coverage often distinguishes between generic and brand-name medications. Choosing a plan with a high drug maximum is a strategic way to protect your long-term savings from the costs of chronic conditions.

Dental services are typically divided into basic preventive care and major restorative work. While most plans cover annual cleanings and fillings, coverage for orthodontics or crowns often requires a higher tier of protection. Vision care also goes beyond simple eye exams; many modern plans now include provisions for laser eye surgery or high-quality hardware. Extended health care provides a final safety net, covering semi-private hospital rooms, specialized nursing, and essential medical equipment. This comprehensive breakdown helps you understand exactly what provincial health insurance doesn't cover, allowing for more precise financial forecasting and peace of mind.

Prioritizing Paramedical and Mental Health Support

In 2026, the demand for mental health professionals such as psychologists and social workers has reached an all-time high. When you compare plans, pay close attention to whether coverage is capped per visit or as an annual combined total for all paramedical services. Many families find that "lifestyle" benefits, including massage therapy and physiotherapy, are their most frequently utilized features. A plan that offers a generous combined total provides the flexibility to use funds where they're needed most at any given time. This adaptable approach ensures your coverage evolves with your family's physical and mental well-being.

Emergency Travel Medical: An Often Overlooked Necessity

Your provincial health card offers very limited protection once you cross the border. Emergency travel medical coverage is a critical addition to any robust health plan. It ensures that a sudden illness while travelling doesn't lead to a financial crisis. It's also important to understand how your insurance coordinates with other sources, such as credit card coverage. A bespoke plan ensures these benefits work together seamlessly. This coordination provides a continuous shield of protection wherever your professional or personal life takes you. You don't want to discover gaps in your coverage while in a foreign hospital.

Evaluating the True Cost: Premiums, Deductibles, and Tax Advantages

Determining the actual value of your coverage requires a methodical look at the numbers. Many people focus solely on the monthly premium, but the "Premium vs. Benefit" ratio is what defines your true return on investment. For a 30-year-old Canadian seeking prescription drug and dental coverage, average monthly costs in May 2026 range between $108 and $204. If you're paying more in premiums than you're receiving in routine care, it's time to refine your strategy. By selecting a plan with a higher deductible or co-payment, you can lower these monthly costs while maintaining a shield against catastrophic drug expenses. This approach ensures your health and dental insurance Canada plan serves as an efficient financial tool rather than a drain on your cash flow.

For business owners, the integration of these plans with Corporate Tax Services is essential. These premiums aren't just costs; they're tax-deductible instruments that reduce your overall corporate liability. When you view insurance through this lens, it becomes a sophisticated way to move funds from the corporation to the family in a tax-efficient manner. It transforms a personal necessity into a corporate advantage. To see how these strategies apply to your specific business structure, you can consult with the experts at Alphaspring Financial Inc.

Health Spending Accounts (HSA): The Modern Alternative

A Health Spending Account (HSA) offers a flexible, "pay-as-you-go" alternative to traditional insured plans. For incorporated businesses, an HSA allows medical expenses to be 100% tax-deductible, turning personal medical costs into a legitimate corporate expense. Many professionals now opt for hybrid models. These combine a basic insurance plan for high-cost drug protection with the tax-efficiency of an HSA for routine vision and dental care. This bespoke arrangement ensures you aren't paying for coverage you don't use while maintaining a robust safety net for your family.

The Medical Expense Tax Credit (METC) Framework

If you pay for your health and dental insurance Canada premiums personally, you may find relief through the Medical Expense Tax Credit (METC). The CRA allows you to claim un-reimbursed premiums as a non-refundable tax credit, provided they exceed the "3% of income" rule or a set annual threshold. This framework ensures that high medical costs don't disproportionately affect your financial stability. The Canada Revenue Agency recognizes private health services plans as a legitimate means of funding medical care when the plan is primarily for the benefit of the individual and their dependants.

Designing Your Bespoke Protection: The Alphaspring Financial Advantage

Choosing the right protection is more than a transaction; it's a strategic investment in your future. While many providers direct you toward a generic digital quote tool, Alphaspring Financial believes that complex planning requires a human touch. A wise guide helps you see the patterns in your financial life that an algorithm might miss. Securing health and dental insurance Canada is just one piece of a larger puzzle. We ensure your coverage is not an isolated expense but a synchronized part of your broader Retirement Planning strategy. This integration prevents medical costs from eroding your nest egg when you are most vulnerable.

Our philosophy centres on the "Living Benefits" ecosystem. This approach recognizes that health and dental insurance must work in tandem with disability and critical illness protection. It's about protecting your quality of life while you're here. We look at how these plans interact with your Life Insurance goals to create a seamless shield of protection. This methodical synchronization ensures that your family's financial legacy remains intact regardless of health challenges. By viewing your needs through this holistic lens, we remove the uncertainty that often accompanies long-term planning.

A Holistic Approach to Risk Management

We begin by analyzing your entire financial picture to identify hidden coverage gaps. High-net-worth individuals and business owners often have unique risks that standard policies ignore. Our team tailors each plan with meticulous care, focusing on stability and foresight. We don't just look at today's premiums. We project how your needs will evolve over the next decade. This commitment to traditional reliability, combined with an innovative perspective on wealth preservation, sets our consultancy apart. You deserve a partner who values your long-term security as much as you do.

Your Next Steps Toward Peace of Mind

Taking the first step toward a secure future is a collaborative process. When you speak with our advisors, expect a structured conversation focused on your life milestones and family goals. We recommend gathering your current benefit details and a summary of your recent out-of-pocket medical expenses before our meeting. This data allows for a more productive review of your current standing. We will help you navigate the fine print and jargon to find the health and dental insurance Canada solution that fits your life. Your journey toward comprehensive protection and quiet confidence starts with a single, informed decision.

Securing Your Future with Strategic Foresight

The structure of Canadian healthcare is evolving. You now understand how to bridge the gap between provincial coverage and your personal requirements. We have explored the strategic importance of choosing between individual and group models, the tax efficiency of Health Spending Accounts, and the necessity of a holistic approach to protection. Securing the right health and dental insurance Canada plan is not merely a medical decision; it's a fundamental step in preserving your wealth and family legacy.

At Alphaspring Financial, we act as your wise guide through these complex financial milestones. Our integrated insurance and tax advisory expertise ensures that every detail of your plan is handled with meticulous care. We provide the reassuring, professional support needed to turn uncertainty into long-term security. You don't have to navigate these choices alone. Your path to quiet confidence and financial stability starts with a single, proactive step.

We look forward to helping you build a resilient future.

Frequently Asked Questions

Is private health and dental insurance worth it if I am healthy?

Maintaining coverage is a strategic move to protect your long-term financial stability. While you may not require frequent care today, insurance acts as a hedge against the sudden, high costs of accidents or unexpected chronic diagnoses. It also provides immediate value through preventive services that help you maintain your current health status and avoid more expensive procedures in the future.

Can I get health insurance in Canada if I have a pre-existing condition?

You can secure protection through "guaranteed issue" plans that do not require a medical questionnaire. These plans ensure that individuals with existing health histories can still access essential benefits for drugs and dental care. While these policies may have different coverage maximums than medically underwritten plans, they offer the certainty that you won't be denied coverage due to your medical past.

How much does the average health and dental insurance plan cost in Canada?

The cost of health and dental insurance Canada varies based on several factors, including your age, province of residence, and the specific level of coverage you select. Plans that include major restorative dental work or high prescription drug maximums will naturally have higher premiums. A tailored consultation can help you find a plan that balances comprehensive protection with a premium that reflects your specific family budget.

Are health insurance premiums tax-deductible for small business owners?

Premiums are typically 100% tax-deductible for incorporated business owners when the plan is structured correctly as a business expense. For self-employed individuals, these costs can often be deducted from business income or claimed as a medical expense tax credit on a personal return. This tax efficiency makes private insurance one of the most cost-effective ways to fund your family's healthcare needs.

What is the difference between a Health Spending Account and traditional insurance?

A Health Spending Account (HSA) is a defined contribution model where you set a specific dollar limit for medical spending each year. Traditional insurance is a defined benefit model that transfers the risk of high-cost claims to an insurance provider. Many professionals choose to combine these two structures to enjoy the flexibility of an HSA alongside the catastrophic protection of an insured plan.

Do I need health insurance if I already have coverage through my employer?

You may still benefit from a personal plan if your employer-sponsored benefits have low maximums or exclude specific services your family requires. It's common for workplace plans to have caps on psychological services or major dental work. Having a secondary plan allows you to coordinate benefits, which can often result in 100% reimbursement for your out-of-pocket medical expenses.

How do I coordinate benefits between my plan and my spouse’s plan?

Coordination of benefits follows a methodical sequence to ensure you receive the maximum allowable reimbursement. You must submit your own claims to your insurance provider first; any remaining balance is then submitted to your spouse's plan. This structured process allows families to utilize the full capacity of both policies, significantly reducing the net cost of healthcare services.

What happens to my health insurance when I retire in Canada?

Most employer-sponsored group benefits terminate on your last day of work, which can leave you vulnerable during a period of increased medical need. You have the option to transition to a "FollowMe" or replacement plan within 60 to 90 days of retirement without undergoing a medical exam. Planning this transition in advance ensures your protection remains continuous and your retirement savings stay protected from rising healthcare costs.